Amazon diversification

Gregory John Lee

Vernon Timothy Thaver

From

Amazon expands past e-commerce to cloud & beyond (1994-2004)

Main area: Coud computing and streaming

Other areas: Business strategy in the digital era

Researched to end 2024

Amazon Case

Amazon has been a giant in the digital world for so long that it is almost hard to remember that they were once a small start-up and then, even after becoming the most famous trailblazer of e-commerce, that they struggled to become profitable for a long time.

This case will discuss the ways in which Amazon used diversification, notably in promising digital spheres, to become profitable, and, then, to become a technology giant. The majority focus of the case will be on their creation of cloud computing through Amazon Web Services; however, more recent plays will also be discussed.

Amazon’s Beginnings in Retail E-Commerce

Famously, Jeff Bezos created Amazon in 1994 out of his garage. Bezos had enjoyed a successful Wall Street career, but having realized the potential of the internet he had wanted to create a business harnessing this oncoming revolution.

Amazon was started as an online bookstore. Famously, the initial company name was “Cadabra”; however, Bezos renamed it when someone mispronounced the name as “cadaver”. He decided to choose a name beginning with the letter A to position it at the top of alphabetic searches, and chose Amazon because, like the river, he wanted the endeavor to be the world’s biggest (Ria, 2023). The initial company grew well within its book sales domain. In addition, the company was rapidly learning how to harness the power of digitalization inherent in e-commerce. For instance, Ria (2023) notes:

Bezos accomplished more than merely establishing a bookstore, he forged an online community. During its early stages, the website was groundbreaking by enabling ordinary consumers to craft product reviews online. This innovation not only attracted individuals seeking to purchase books but also those keen on researching them before making a purchase.

The next step was for Amazon to diversify beyond books, which they did steadily over the years after establishing themselves, with the introduction over the late 1990s of videos, music compact disc, video games, electronics, toys, home improvement items, and software (McFadden, 2023).

As noted in the Walmart case study (Case 20 from p. 239); however, Amazon was increasingly competing against the brick-and-mortar retail giants. These established giants had marked advantages at the time: they offered incredibly wide stock ranges (including fresh food), great pricing, and consumers could get what they wanted quickly (Amazon’s deliveries were still comparatively slow and, for instance, Case 20 notes that Walmart was said to have a presence within 10 minutes of 90% of Americans).

The bigger it got, the more that Amazon was forced to play catch-up to the Walmarts of the world. They worked tirelessly from the late 1990s to the mid-2000s on expanding their range, speeding up delivery, and achieving competitive or even superior pricing:

- Amazon widened their range by developing increasingly wide and advantageous supply chains but also welcoming in third party sellers and Amazon Marketplace in the early 2000s (Ria, 2023), which turned them into a true platform business and essentially created a near-automated method of achieving supply growth potential. Later, with Amazon Fresh, the company introduced fresh foods, which was a major differentiator for traditional retailers before that.

- Delivery improvements were achieved in various ways. Amazon worked with logistics services more closely, for instance, they negotiated a highly advantageous deal with the US Postal Service (USPS) in 2006 which allowed them better delivery to rural areas and considerable delivery capacity (Scott, 2024). Perhaps most importantly, the company created Amazon Prime in 2005, which offered better delivery times and other advantages to paid monthly subscribers. Over the past decade, delivery for Prime members has been brought down to as little as same-day or one-day delivery. Part of this success was constant efforts to build distributed, industry-leading, efficient and increasingly automated warehouse facilities.

- As Amazon became larger and worked harder on supply chain agreements and marketplace guidance, their prices also became competitive with large retailers. A large part of this was cost control. One cost control area was their warehouses, which are run by workforces who are poorly paid, aggressively and in some cases possibly unethically performance managed (Kantor & Streitfeld, 2015; Peters, 2021; Winkie, 2022) , and traditionally non-unionized . Increasing warehouse automation has also streamlined cost .

- Amazon also expanded to international markets between the late 1990s and early 2000s, and has increasingly continued to do so with localized strategies (e.g., Lino, 2024). This expansion allowed them to diversify revenue streams and achieve additional scales of economy.

- In the 2010s, Amazon started to expand into brick-and-mortar stores with the acquisition of Whole Foods and the building of their Amazon Go stores. This was an effort to erode the last remaining unchallenged advantage retained by the likes of Walmart: physical presence.

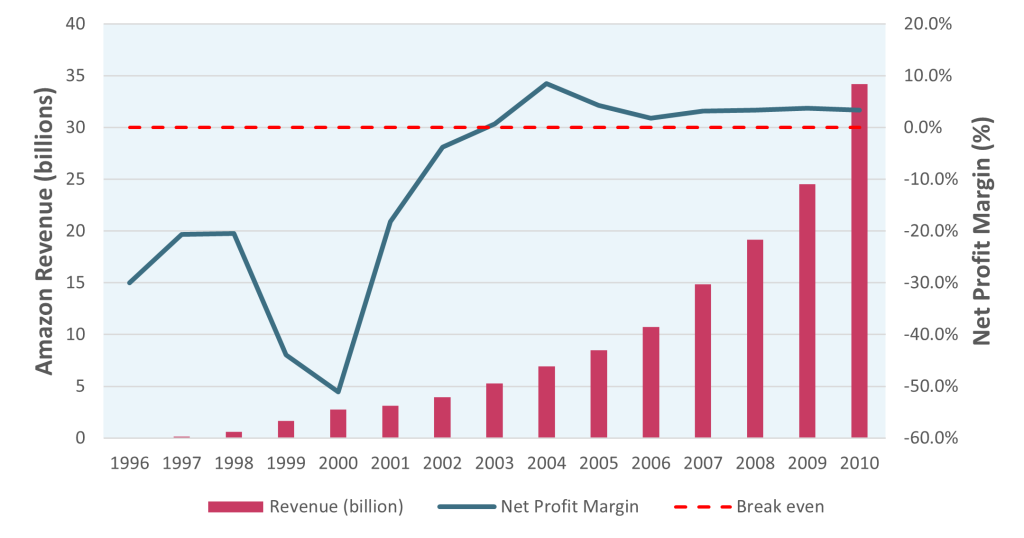

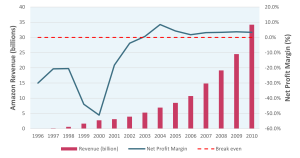

By 2000, Amazon was achieving revenues of over $2 billion and were enjoying rapid growth. However, as seen in Figure 1, they were famously unprofitable for nearly their entire first decade, incurring profit losses on the initial revenue growth.

Figure 1: Amazon revenue and net profit margin 1996-2010

Sources: Dazeinfo (2020a & b); net profit margins calculated by author

It was only in 2003 that they started becoming profitable, with operating income of $35 million off a $5 billion revenue base.

Investors had become restless in this first unprofitable decade, and Amazon was under pressure to improve its position. It was in this climate that they began to diversify from being an e-commerce retailer to something far broader: a technology firm. This journey started with Amazon Web Services, which we discuss next.

Amazon’s Creation of AWS Cloud Computing

Amazon Web Services (AWS) is not only a behemoth in the world of cloud computing; it essentially created the industry.

AWS is the most used cloud computing service in the world, and it competes with Microsoft Azure for the position as most profitable global cloud service (Haranas, 2024). AWS is the cornerstone of Amazon’s overall profitability, currently accounting for some three quarters of their operating income (Coppola, 2024). This section of the case study explores not only Amazon’s genesis of the cloud computing idea, but its ongoing journey as the field becomes saturated with serious competition.

The History of AWS

Conceptualized between 2002 and 2003, AWS began as an idea to structure Amazon’s own internal information technology infrastructure in a way that could be commoditized as a service. The idea was, therefore, to rent Amazon datacenter server capabilities – such as computer storage or processing – to other organizations at a cost that would be lower than the customer could achieve by having their own datacenters.

The first version was developed and launched in Cape Town, South Africa, in 2004, with the expanded service renamed to Amazon Web Services in 2006. The service was an overnight success. By 2007, over 180,000 developers had joined AWS. In 2010, the service took over the core business of running Amazon.com retail web services.

This success required the development of bigger and more complex datacenters around the world. Figure 2 shows an example of server stacks in a modern AWS datacenter.

Figure 2: Server stacks in a modern cloud computing datacenter

Of course, all was not plain sailing for AWS. A first major hiccough occurred in 2011 when some parts of the service froze and were unable to process requests for two days (Svensson, 2011). In the following year, major customers such as Pinterest, Reddit, and Foursquare also experienced serious issues (Ludwig, 2012). Since these early problems, a growing array of technical complexity keeps AWS developers constantly challenged to maintain high levels of connectivity and functionality. Another challenge has and continues to be cybersecurity. Hacking is, unfortunately, a constant concern in the public cloud space. In a major cybersecurity breach, Techmonitor (2020) reports that:

A sophisticated hacker group pwned Amazon Web Services (AWS) servers, set up a rootkit that let them remotely control servers, then merrily funneled sensitive corporate data home to its command and control (C2) servers from a range of compromised Windows and Linux machines inside an AWS data center.

Such cybersecurity challenges are certainly not unique to AWS; it is an industry-wide problem (e.g., Joshi, 2024). However, cloud security presents concerns to customers and is leading to certain changes in cloud use such as the increasing use of hybrid cloud in which customers blend public and private cloud elements.

AWS and the 4IR Cloud Frontier

The future is exciting for major cloud services like AWS. For example, in 2017, AWS released a host of AI services to the market, which doubled their revenue. Other 4IR services have also been released, and the latest wave of 4IR implementations – notably AI growth –has also led to a major 2024 growth in Amazon financial success (e.g., Sawalka, 2024). AWS also began to serve as a hub for cloud computing knowledge sharing. From 2012, they have organized major conference events (Amazon.com, 2012) and in 2013 began offering certifications in cloud computing and engineering (Amazon.com, 2013). In 2018, AWS launched an artificial intelligence and machine learning certification (e.g., Calhoun, 2018).

AWS Financial Trajectory

By 2021, AWS raked in $96 billion in revenue for Amazon, and accounted for 74% of their profits (Ali & Lam, 2022). Their 2024 projections for revenue have reached $110 billion (Haranas, 2024).

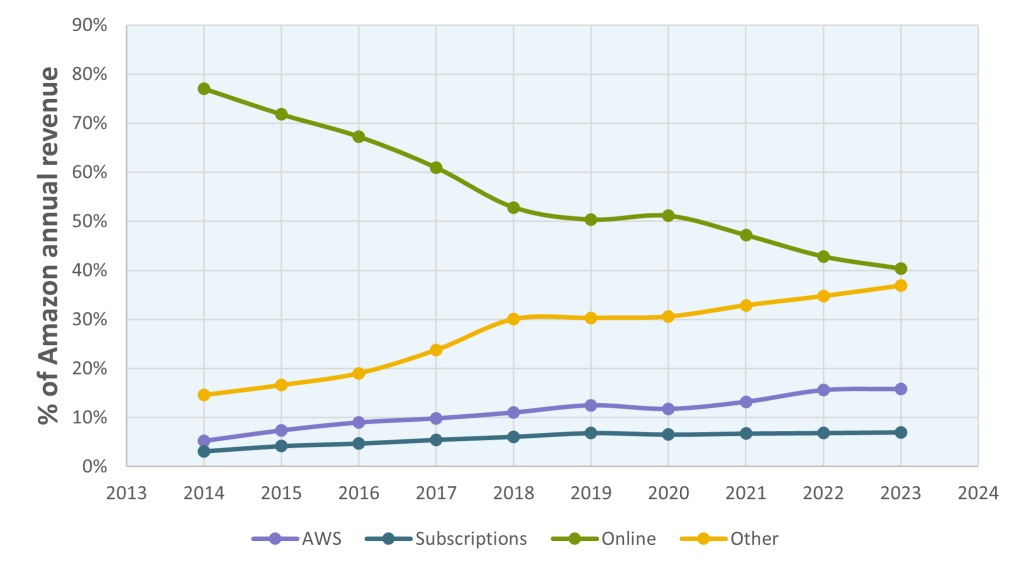

As a result of their first-mover advantage and constant innovation, AWS has formed a gradually growing proportion of Amazon net annual revenue, as seen in Figure 3 (although as seen there, the real growth has been in alternative revenues which are recently dominated by Amazon’s rapidly increasing advertising revenue).

Since AWS hosts the majority of the other revenue streams like subscriptions, its group contribution is far higher than that seen in Figure 3. Some of these newer services are discussed further below.

Figure 3: AWS percentage of revenue by segment 2013-2023

Sources: Coppola (2024); Curry (2024)

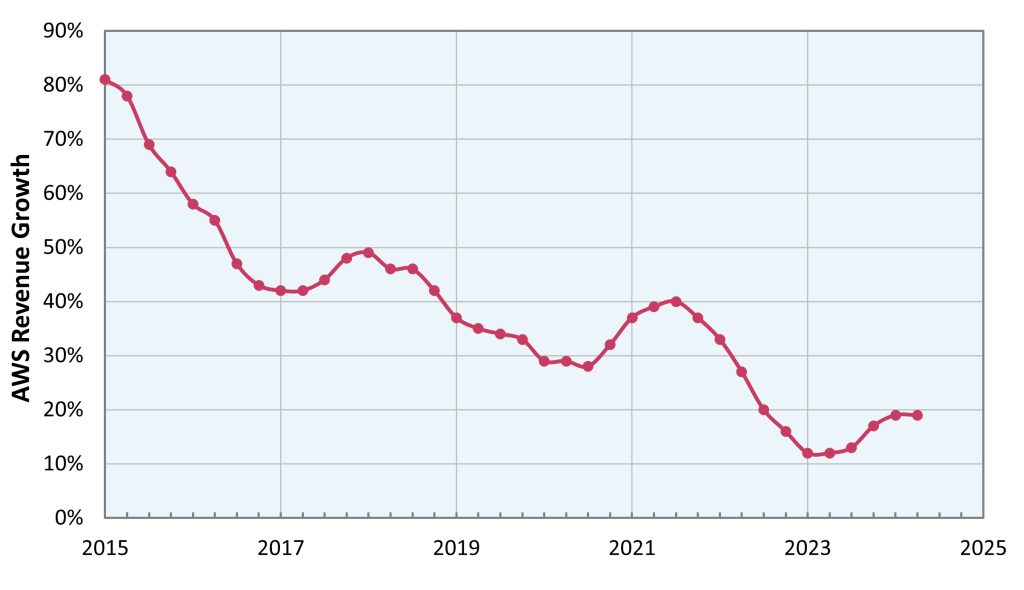

However, although AWS revenues and profits remain stellar, notably in an excellent 2024, they have overall declined in growth as seen in Figure 4.

Figure 5 4: AWS revenue growth 2015-Q3 2024

Sources: Amazon.com (2024); Vailshery (2024)

This decline is largely due to the rapid growth in cloud computing competitors as discussed further below.

Increasing Competition in the Cloud Space

Notwithstanding AWS’s first-mover advantage and ongoing success, the competitive environment has steadily intensified.

Competition among Western Cloud Computing Companies

AWS’s biggest rivals, Microsoft’s Azure and Google Cloud, have been gaining market share since 2016 while AWS has been losing share. In 2019, this competition would intensify due to Microsoft’s acquisition of the giant Pentagon JEDI contract (worth up to $10 billion on its own); although, due to a legal battle incited by Amazon, this contract was cancelled and replaced with a $9 billion contract split between Amazon, Microsoft, Google, and Oracle (Gomes & Stone, 2022; Gregg & Greene, 2021).

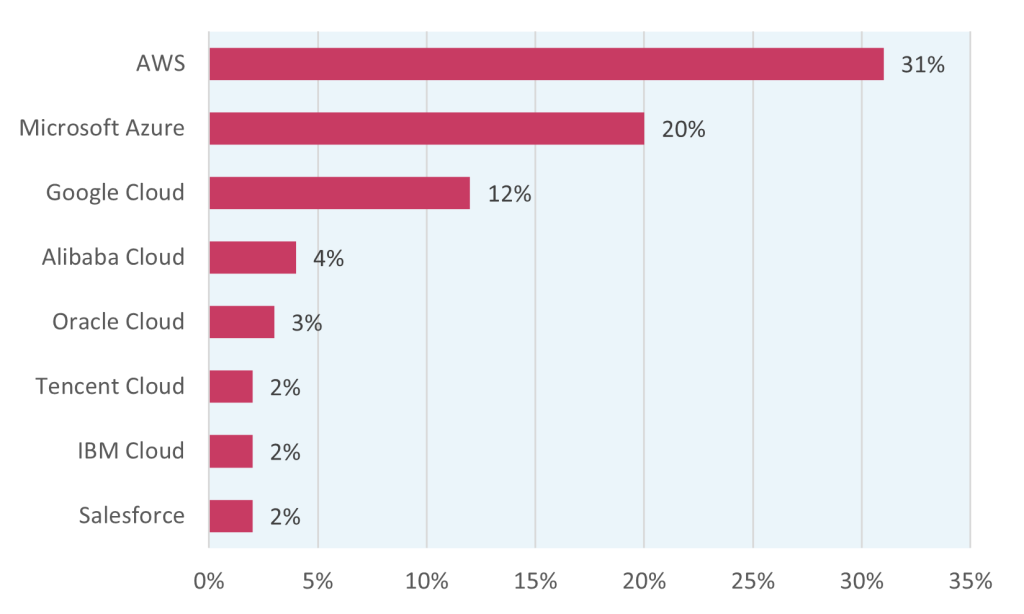

Figure 5 shows the share of market as of Q3 2024. Amazon retains a commanding one third share; however, the closest rivals, Microsoft and Google, continue to grow into double digit market share.

Figure 5: Percentage of worldwide cloud computing market, Q3 2024

Source: Richter (2024)

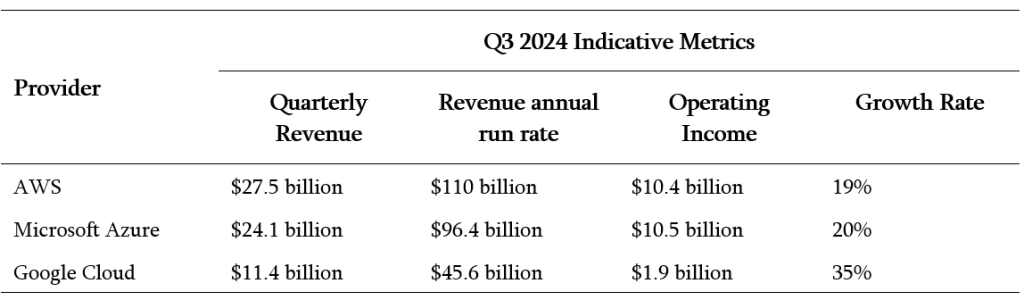

In terms of financial metrics, Table 1 provides indicative information for the big three cloud providers as of Q3 2024. As seen there, AWS and Azure remain close at the top; however, growth momentum is more with the likes of Google at the moment.

Table 1: Q3 2024 revenue, run rate, operating income & growth of the big 3 cloud providers

Source: Haranas (2024)

An interesting market segment concerns the Chinese technology giants and the Eastern market centered around China. We can see in Figure 5 that Alibaba and Tencent together only command 4% and 3% of the world market respectively; however, the following section discusses their local geographical relevance.

AWS in the Eastern Market

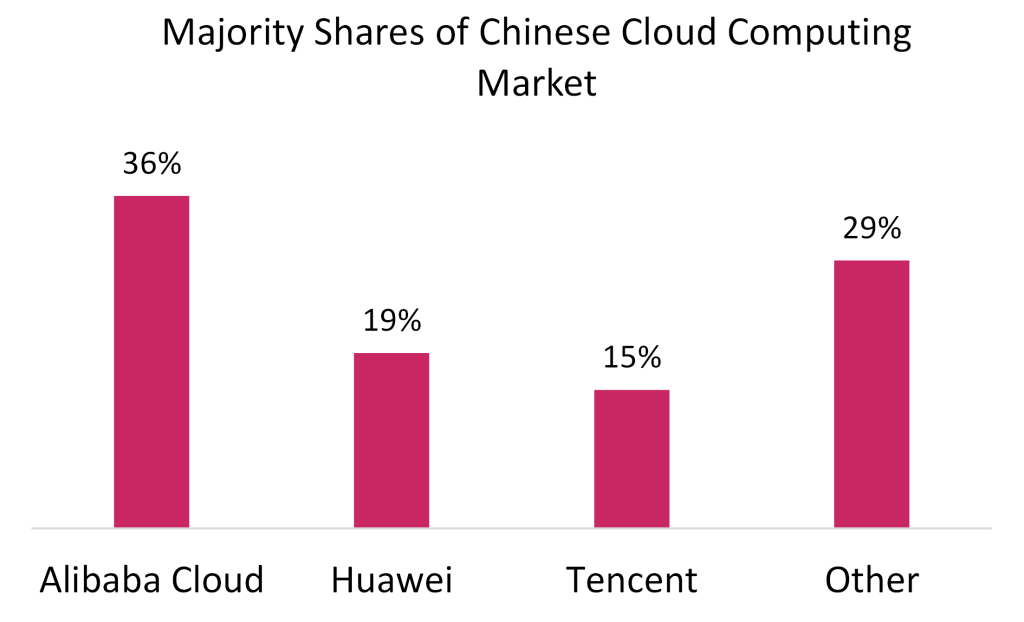

Notwithstanding the overall dominance of AWS and Microsoft along with a variety of other US-based technology giants, their control of the market is not geographically ubiquitous. This is most noteworthy in China, which has successfully erected thickets against most American technology giant dominance. This is also true in cloud, where three Chinese companies control 70% of the market, as seen in Figure 6.

Figure 6: Share of the cloud market in China as of Q3 2024

Source: Canalys (2024)

China’s cloud market started slowly, but recently has blossomed, with $10.2 billion in revenue and double-digit growth (Canalys, 2024). Although this remains a relatively small market (comparable to the quarterly operating income of Azure alone), the growth is expected to remain high.

It is evident that the early achievement of scale by local players may establish footholds endure even should US players gain more ability to attack this market.

Another thing to consider is what occurs when major tech giants first establish local hyperscale presences in smaller economies, such as developing or emerging nations.

Penetration of Hyperscale Players in Developing Markets (South Africa as Example)

Hyperscale cloud players such as AWS have increasingly started to establish serious presence in certain key developing countries. One example considered here is South Africa.

Prior to about 2020, South Africa was a good example of the state of cloud computing for a developing nation. Cloud customers had choices between smaller, local cloud players who typically served customers with reduced capacity cloud services, such as IaaS-based options without features such as metering or elasticity. Customers often accessed larger players offshore; however, this had severe limitations due to factors such as regulatory restrictions in moving certain data across national boundaries and the cost and difficulty of long-distance data movement.

However, after this, several large cloud organizations announced the development of substantial cloud capacity within the country. Microsoft launched enterprise-grade cloud centers in Johannesburg and Cape Town in 2019, and AWS developed a cloud center in Cape Town, which fully launched in April 2020. Huawei developed cloud capacity within the country, Oracle announced large future investments, and Google began working with a local player to offer Google Cloud and also began laying an undersea cable to the country. Some of these investments were curtailed by COVID-19, but many have gone ahead.

There are probably several reasons for the entry of the international giants. First, South Africa is the most advanced and second largest economy on the continent, providing a potential starting point for entry into Africa. In addition, as mentioned above, regulation and practicality constricted the ability of South African companies to use international cloud centers (with impending regulation only providing further restrictions).

What does the increased presence of major players mean for the established, smaller cloud players in countries such as South Africa? One view is that they would be destroyed, unable to compete with the cost, feature, and other advantages of the likes of AWS. However, there is a compelling countervailing view that local players may still have a strong role to play in several ways.

The increased need for hybrid or private cloud models presents a role for well-equipped local players. For customers desiring some on-premise or dedicated managed infrastructure, the private elements could still be set up and managed by local players.

In addition, there should be substantial advisory services work in helping customers with elements such as which of their needs to cede to public cloud (and to whom, since multi-cloud options are available) and which to retain in more private environments if desired. Setting up multi-cloud integration portals (“single panes of glass”, as discussed above) is also a possible activity.

Assistance with migrations and specific feature programming in FaaS are other potential areas for local expertise.

However, certainly, the arrival of large hyperscale players into geographical zones not already dominated by equivalent first-movers, as occurred in China, is likely to lead to domination by players like AWS. For geopolitical and economic reasons, countries not yet dominated by large hyperscale players may wish to consider whether they can develop the likes of a local Alibaba or Tencent.

Conclusion on AWS

As the first major diversification of Amazon, and almost certainly its most groundbreaking, AWS not only changed the face and fortunes of the company but of the fourth industrial revolution. AWS continues to evolve. As reported by Cohan (2020), the cloud arm is attempting to keep doing so through a combination of thought leadership, exemplary talent acquisition , customer experience management and research, and deep analytical understanding of its business.

Regardless of the precise future of AWS, the overall cloud computing market has been a major fillip for organizational computing since the groundbreaking 2006 Amazon launch. Cloud computing is expected to continue growing with its capability of bringing 4IR technologies such as RPA, AI, IoT and many others to customers easily and affordably.

Subscription Services Tiered on Top on AWS

Besides the cloud services and e-commerce that Amazon is renowned for, a growing portion of their revenue originates from their subscription services, which include Amazon Prime and Audible. Amazon Prime Video (the company’s streaming service) is a modest revenue stream in comparison to Amazon’s other exploits, but still wracks up more than 200 million monthly viewers (Spangler, 2024).

An advantage that Prime Video holds above other streaming services is a willingness to invest in novel content, where the site is used to extract user behavior and feedback on pilot projects (McDuling, 2015). Interestingly, Amazon does not appear to be competing with other streaming services, opting instead to use Prime Video to encourage online retail shopping, functioning more as a “loss-leading end cap” (Csathy, 2020).

Despite this original purpose, now-CEO Andy Jassy believes that Prime Video could be a successful standalone business venture (Spangler, 2024).

Amazon’s Home Automation Endeavors

Amazon has also created a string of home automation business lines, notably the combination of the Amazon Alexa AI-driven software and the Echo devices, but also including Ring, Dash, and others. These home automation endeavors are extensively discussed in another case study in this collection and so are not discussed further here.

Advertising Strategy

In 2024, Amazon implemented an ad-inclusive strategy, though this was largely unwelcomed by users (Tassi, 2024). Within their streaming services, the advertising is now increasingly prominent, and subscribers have to pay to opt out. Amazon is set to further increase the number of advertisement slots in 2025 (Thomas, 2024).

From January to March, Amazon’s revenue from advertisements increased by 24% year-on-year (Labiak, 2024). According to Yuen (2024), Amazon was estimated to earn $4.72 billion from ads in 2024, accounting for 11.2% of Amazon’s total advertising revenue. As noted previously, advertising revenue is the standout growth factor in the “Other” category in Figure 3.

Advertising is relatively unconnected to AWS, aside from its role in hosting the subscription services. However, this move is indicative of Amazon’s desire to continue looking for new revenue streams beyond e-commerce and cloud.

Amazon and AI

Amazon has a long history, spanning over 20 years, with artificial intelligence (Madia, 2022). The company’s focus on AI has grown even further over the 2020s, with big investments being made into this technology set (e.g., Satariano, 2024; Varghese & Srivastava, 2025). The implementation of AI thus far has resulted in major shifts in Amazon’s business, including improving customer assistance and fit recommendations.

According to Doug Herrington, CEO of Amazon Worldwide Stores (Berg, 2025):

AI is becoming transformative for our business, and we haven’t had a technology revolution as large as this since the start of the internet.

Recently, Amazon has implemented AI in several ways. For instance, at the end of January 2025, it will retire its “Try Before You Buy” program (a feature of Prime Wardrobe), which allowed customers to order a limited number of items, try them on at home, purchase the items they want, and return the others. This retirement is a result of virtual try-ons, an augmented reality feature that enables customers to see how they would look in items, with an AI-powered tool that offers personalized size recommendations that are based on the customers’ purchase and return patterns, as well as other customers’ feedback. This would ideally reduce the number of items returned under Amazon’s free-return policy. Along with this, customers can engage with Rufus, a generative AI assistant that was released in February 2024 (Berg, 2025; Schwartz, 2025b).

Amazon had a major advantage over its rivals regarding smart speakers with releases like Alexa, as discussed further in Case 9 on p. 121. The company now plans to overhaul its current question-answering engine and replace this with in-house generative AI models (Schwartz, 2025a). These generative AI models debuted in late 2024 and may be a game-changer, as they combine cutting-edge technology with affordability, being 75% cheaper than other Amazon Bedrock models (Abbas, 2025). However, it remains to be seen whether Alexa’s upgrade will be chosen over other options like Gemini and ChatGPT which have already been released (Schwartz, 2025a).

Despite these innovations, the actual adoption of AI technologies appears to be lagging. Amazon’s 2024 State of Procurement report states that 96% of leaders plan to invest in AI (with 32% being interested in exploring deeper data analytic capabilities), but the major focus has been placed on tools that will tackle short-term cost pressures, delaying the use of AI for transformative purposes (Chapman, 2025). However, HSBC analyst Christopher Johnen predicts that AWS’s cloud-computing division could add about $20 billion to Amazon’s revenue in 2025, adding that generative AI will likely be a big player in increasing growth compared to 2024 (Glover, 2025).

Autonomous Vehicles

An additional Amazon foray has been into autonomous vehicles, which they first started in 2015 (Weinberg, 2020). In 2020, the company bought Zoox, an autonomous-vehicle startup (Lombardo & Higgins, 2020). Test drives of the vehicles started in early 2023 (The Guardian, 2023). According to CTO Jesse Levinson, rides will hopefully be offered to the public “quite soon” (Wayland, 2025). Deichmann et al. (2023) estimate that the revenue of the global robotaxi market could bring in roughly $1.3 trillion by 2030 (Fujita, 2024), explaining Amazon’s interest in the market. Zoox’s vehicles differ from those of other self-driving companies, as its vehicles are designed with a completely driverless-first approach (Fujita, 2024). Along with generating revenue, investing in autonomous vehicles could reduce Amazon’s massive transportation costs (reported as $27.7 billion in 2018), which have quickly increased due to their fast delivery times (Weinberg, 2020). Therefore, this foray into autonomous driving could have significant complementarities with their retail arms.

Amazon Case: Conclusion

In the face of increasing competition, Amazon has continued to find new, innovative ways to thrive through judicious and often groundbreaking diversification.

Challenges to the Reader: Amazon Diversification

Applying the Ansoff matrix to successive Amazon strategies

In the case study, we see the rough timelines of developments and strategies at Amazon as follows:

- 1994-1998: Initial launch as an e-commerce bookstore.

- 1998-2004: Expansion from books to other increasingly broad consumer goods, and exploring free shipping memberships and the like. Also: expanding to international markets.

- 2005-2011: Expansion into cloud computing. Keeps expanding e-commerce too.

- 2011-: Creates other services like streaming and household automation.

Align each of these strategies with the Ansoff matrix (see, for instance, this explanatory video) to describe what type of strategic approach it was, and consider the level of risk potentially involved for Amazon.

Disruptive innovation perspective on the Amazon case

By the early to mid-2000s, Amazon were still disruptive innovators trying to upend the established US retail giants such as Walmart as well as trying to forge new pathways, as we have seen in this case. Amazon had created an entry foothold as an e-commerce disruptive innovator, but this case has shown that by the early 2000s, they not only needed to scale to meet the incumbents, but they also needed to find new sources of profit to stay alive after an initial decade of unprofitability.

Use the material in our disruptive innovator entry and scaling perspectives download to consider the following questions:

Use the Venn diagram tool to analyze early-2000 Amazon’s competitive position

Use the Venn diagram competitive analysis tool for disruptive innovators (Figure 1 in the document) to analyze Amazon as a disruptor versus incumbents at the time such as Walmart. Note that you may not be able to fill in elements for all points/zones in Figure 1, notably, you should focus on points 1-2 and 6-7.

Scaling strategies for early-2000 Amazon’s competitive position

How do the diversification strategies by Amazon fit in with the scaling strategies for disruptive innovators (Figure 3 in the document)?

Reflections on the Challenges

Reflection on applying the Ansoff matrix to successive Amazon strategies

Using this explanatory video (or similar sources) to describe the types of strategic approaches taken by Amazon over time, and the level of risk potentially involved for Amazon, gives us the following.

Recall that the rough progression of Amazon business lines / strategies over time was as follows:

- 1994–1998: Initial launch as e-commerce bookstore.

- 1998–2004: Expansion from books to other increasingly broad consumer goods, and exploring free shipping memberships and the like. Also: expanding to international markets.

- 2005–2011: Expansion into cloud computing. Keeps expanding e-commerce too.

- 2011-: Creates other services like streaming and household automation.

We can assess these evolutions in terms of the Ansoff matrix as per Figure 7:

Figure 7: Early 2000s Amazon strategies aligned to the Ansoff matrix

Reflection on the disruptive innovation perspective on the Amazon case

This reflection is reserved for teaching purposes.

References: Amazon Diversification

Abbas, A. (2025, Jan 17). Amazon Nova Foundation Models: Redefining price and performance in generative AI. Unite.AI.

Ali, A. & Lam, S. (2022, Jul 10). AWS: Powering the internet and Amazon’s profits. visualcapitalist.com.

Amazon.com. (2012, May 9). Amazon Web Services announces first global customer and partner conference: AWS re: Invent.

Amazon.com. (2013, Apr 30). Amazon Web Services announces launch of certification program for AWS cloud computing professionals.

Amazon.com. (2024, Oct 31). Amazon.com announces third quarter results.

Berg, N. (2025, Jan 12). Amazon Stores CEO says AI may spawn new retail formats. Forbes.

Calhoun, C. (2018, Dec 6). New AWS training and certification offerings for machine learning and re:Invent launches. AWS.

Canalys. (2024, Dec 24). Mainland China’s cloud service spend grew by 11% in Q3 2024.

Chapman, T. (2025, Jan 13). Amazon Business: AI and ESG taking procurement backseat. SupplyChain.

Cohan, P. (2020, Jan 6). How much of Amazon’s $7.3 billion AWS profit will rivals win? Forbes.

Coppola, D. (2024, Jul 30). Amazon operating income 2014-2023, by segment. Statista.

Csathy, P. (2020, Jan 31). Amazon Prime Video: The stealthy, ominous streaming force. Forbes.

Curry, D. (2024, Nov 5). Amazon statistics (2024). Business of Apps.

Dazeinfo. (2020a, Apr 13). Amazon revenue vs net income by year.

Dazeinfo. (2020b, Apr 13). Growth in Amazon revenue by year.

Fujita, A. (2024, Oct 11). Why Amazon’s Zoox is taking a different approach to autonomous taxis. Yahoo! Finance.

Glover, G. (2025, Jan 13). Amazon stock can jump 23%, analyst says. Why it’s all about AI. Barron’s.

Gomes, N. & Stone, M. (2022, Dec 8). Pentagon splits $9 billion cloud contract among Google, Amazon, Oracle and Microsoft. Reuters.

Gregg, A. & Greene, J. (2021, Jul 6). Pentagon cancels $10 billion JEDI contract challenged by Amazon, ending long-contested cloud-computing deal. The Washington Post.

Haranas, M. (2024, Nov 4). AWS vs. Microsoft vs. Google Cloud Q3 2024 earnings face-off. CRN.

Joshi, A. (2024, Sep 10). These sectors are top targets for cybercrime, and other cybersecurity news to know this month. World Economic Forum.

Kantor, J. & Streitfeld, D. (2015, Aug 15). Inside Amazon: Wrestling big ideas in a bruising workplace. New York Times.

Katz, B. (2021, Feb 24). Why Amazon Prime Video doesn’t need to beat Netflix or Disney+. Observer.

Labiak, M. (2024, May 1). Amazon Prime ads help tech giant drive profits. BBC.

Lino, G. (2024, Sep 9). The complete Amazon company history timeline: A guide to the e-commerce giant’s journey. girolino.com.

Lombardo, C. & Higgins, T. (2020, May 26). Amazon in advanced talks to buy self-driving car tech company Zoox. Wall Street Journal.

Ludwig, S. (2012, Jun 29). Amazon cloud outage takes down Netflix, Instagram, Pinterest, & more. VentureBeat.

Madia, K. (2022, Sep 30). Celebrate over 20 years of AI/ML at Innovation Day. AWS.

McDuling, J. (2015, Jan 21). The secret to Amazon’s success in streaming TV. Quartz.

McFadden, C. (updated 2023, Mar 17). A very brief history of Amazon: the everything store. Interesting Engineering.

Peters, B. (2021, Apr 14). A closer look at Amazon: Are unethical working conditions on the rise? The Geopolitics.

Poffringa. (2022, Nov 2). Hyperscaler Q3 2022 Earnings Review. softwarestackinvesting.

Protalinksi, E. (2020, Jul 30). Amazon reports $88.9 billion in Q2 2020 revenue: AWS up 29%, subscriptions up 29%, and ‘other’ up 41%. VentureBeat.

Ria, A. (2023, Oct 31). A brief history of Amazon. Future Startup.

Richter, F. (2024, Nov 1). Amazon maintains cloud lead as Microsoft edges closer: Cloud infrastructure market. Statista.

Satariano, A. (2024, Nov 22). Amazon invests $4 billion in Anthropic, deepening its A.I. ties. New York Times.

Sawalka, V. (2024, Dec 31). Amazon rises 45.6% in 2024: Will AWS & AI innovation fuel 2025 rally? Yahoo! Finance.

Schwartz, E. H. (2025a, Jan 15). Amazon’s upcoming Alexa AI brain transplant might make you use it for more than just weather and timers. TechRadar.

Schwartz, E. H. (2025b, Jan 18). Amazon thinks AI helping you buy clothes is better than you sending back whatever doesn’t fit. TechRadar.

Scott, C. (2024, May 7). Does Amazon deliver through USPS? (Yes, and here’s why it matters). ExpertBeacon.

Sherman, N. & Fleury, M. (2023, Jan 24). Amazon union fight continues despite workers’ win. BBC.

Slotta, D. (2024, Oct 18). China’s cloud infrastructure service market Q4 2019-Q2 2024, by company. Statista.

Spangler, T. (2024, Apr 11). Prime Video now reaches more than 200 million monthly viewers, TV ads ‘off to a strong start,’ Amazon CEO says. Variety.

Svensson, P. (2011, Apr 29). Amazon apologizes for server outage, offers credit. Phys.

Tassi, P. (2024, Apr 2). Amazon Prime Video’s forced ads are an unwelcome surprise. Forbes.

Techmonitor. (2020, Mar 3). Rootkit in the cloud: Hacker group breaches AWS servers.

The Guardian. (2023, Feb 14). Amazon deploys fleet of self-driving robotaxis on California streets.

Thomas, D. (2024, Oct 2). Amazon to increase number of advertisements on Prime Video. Financial Times.

Vailshery, L. S. (2024, Oct 30). Amazon Web Services: year-on-year growth 2014-2024. Statista.

Varghese, H. M. & Srivastava, V. (2025, Jan 8). Amazon’s AWS to invest $11 bln in Georgia to boost AI infrastructure development. Reuters.

Wayland, M. (2025, Jan 17). Why 2025 is set to be a crucial year for Amazon’s Zoox robotaxi unit. CNBC.

Weinberg, N. (2020, Apr 2). Amazon moves into autonomous vehicle market. TechTarget.

Winkie, L. (2022, May 10). Exhausted workers, polluting journeys: how unethical is next-day delivery? The Guardian.

Yuen, M. (2024, Jun 12). How Amazon Prime Video and Netflix are balancing subscription and ad revenue. EMARKETER.

Zahn, M. (2024, Dec 13). Amazon workers authorize strike at company’s first-ever unionized warehouse. ABC News.

Other Titles